Stock Market Wipeout… Bank Closures… Hyperinflation… Currency Collapse… Government Surveillance…

Protect Your Money Now!

… Or Kiss It GOODBYE!

- Will Your Savings Survive a Global Banking Wipeout?

- What Happens When the U.S. Sees Hyperinflation?

- What If Taxes Soar Not Only for the "Rich"?

- Can You Survive If the Stock Market Doesn’t Bounce Back?

The Feds are going to be furious when they see this report!

That’s because they want you to believe that everything is under control… your bank and all your savings safe and secure….

But the truth is, America is in serious trouble.

- U.S. banks are going bankrupt before everyone’s eyes—over 300 have failed in the past two years alone. And more than 1 out of every 10 banks remain at risk...

- The Federal Deposit Insurance Corporation (FDIC) insurance fund is already $7.47 billion in the red... and at the current rate of bank failures, could reach $100 billion in debt by 2013.

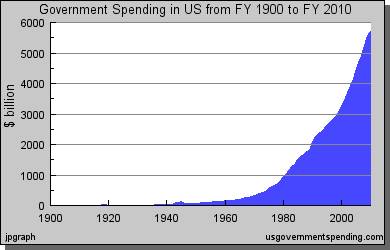

- Excess government spending to the tune of $7.4 trillion is set to skyrocket inflation, putting even basic necessities out of reach for many Americans.

-

All while power-mad government snoops quietly monitor your bank accounts… brokerage accounts… and credit card purchases.

Let Me Help Protect You and Your Family from the Coming Dark Age!

Find out Practical Strategies for Protecting Your Family from the Worst Financial Crisis in 100 Years…

Dear Fellow American,

My name is Bob Livingston, editor of The Bob Livingston Letter®.

I am writing to you because I am convinced that the U.S. is now facing some of the most serious economic and political threats in its history.

After nearly 30 years of unprecedented prosperity, the U.S. economy is now in a shambles.

Millions of Americans have lost their homes… their life savings… and their jobs.

While the U.S. military remains the most powerful force in the world, the most immediate threats America now faces are closer to home:

… failing banks…

… soaring government spending that will lead to

hyperinflation…

… runaway taxes…

… an increasingly totalitarian government that believes in illegal surveillance of law-abiding citizens…

… older citizens no longer able to retire and live what used to be known as their "golden years.”

Fortunately, you DON’T have to just sit by and do nothing. There are simple, easy, inexpensive steps you can take right now to protect your family.

I’ve prepared a 21st-Century Survival Guide called Surviving a Global Financial Crisis and Currency Collapse that I believe can help you prepare for the worst financial threats America now faces.

This manual is chock-full of proven strategies, techniques and information that can make all the difference in a financial emergency.

In fact, Surviving a Global Financial Crisis and Currency Collapse will actually make your life better even if, God willing, we sidestep some of the economic catastrophes that I fear are coming.

That’s because the steps you take now to prepare for some of these possible disasters will end up making you financially stronger… more independent… and more self-reliant than you are now.

You won’t find this privately printed dossier in stores. I’ve developed it exclusively for my extended family of readers, and packed it with practical, real-world strategies for coping with a financial catastrophe.

Continued below...

Get FREE Urgent Alternative Health and

Wealth Alerts from Personal Liberty Digest.

Plus, weekly breaking news updates

and political commentary you won't find

in the mainstream media including…

- Breaking health discoveries and low cost treatments you'll never hear from your M.D.…

- Money-making and money-saving investment tips your broker would never tell you about…

- Privacy and Asset Protection strategies the government hopes you'll never learn…

- Plus, much, much more!

To get FREE Alerts from Personal Liberty Digest™ delivered to your inbox, just fill in your name and email address below:

Your personal information is as important to us as it is to you. We will never rent, sell or trade your personal information with anyone. You may opt-out of alerts from Personal Liberty Digest™ at any time.

Let me give you one example…

Protect Your Savings from Failing Banks

America's biggest banks are running to the Federal government for emergency loans and bailouts. Hundreds of financial institutions have already gone belly up in the past two years. And hundreds more could fail in the months ahead.

Yet the FDIC's Deposit Insurance Fund (DIF) is already out of money.

Despite a $52.4 billion surplus in 2007, the FDIC's fund is now over $7.4 billion in the hole. And at the current rate of bank failures, it could reach $100 billion in debt by 2013.

By the close of 2010, the FDIC had compiled a list of 884 problem banks. That means more than one out of every ten banks insured by the FDIC is in trouble.

So even though Washington wants you to believe everything is just fine ... that the economy is well on the way to a full recovery ... the truth is this problem isn't about to fix itself anytime soon.

Some of these banks will survive. But many won't. Experts like Zacks Investment Research predict hundreds of banks will fail in the coming years—brought down by wave after wave of commercial loan losses.

And that's bad news if your money is in one of these banks.

Because when your bank fails, you don't get a courtesy call or notice in the mail. The Feds close it down without advance notice. It's policy. You show up at the bank to make a withdrawal and the doors are locked shut.

There is usually a notice on the door instructing depositors how they can gain access to their money.

That's what happened to depositors at Colorado National Bank in March 2009. The bank issued a notice telling depositors that their money had been transferred to Herring Bank of Amarillo, Texas.

There are usually few delays in gaining access to your money—usually but not always. And do you really want to take that chance?

When IndyMac Bank of Pasadena, Calif., failed in July 2008, the second-largest bank failure in U.S. history, angry depositors lined up around the block trying to get their money. Many were turned away.

Police threatened anxious customers to remain calm or they would be arrested. It was estimated that 10,000 depositors had as much as $1 billion in uninsured IndyMac accounts.

Continued below…

Feds Plot to Make Foreign

Bank Accounts Illegal

For American investors worried about the safety of U.S. banks, it will soon be too late to seek an alternative.

That’s because some in Congress have plans to make it virtually illegal for an American citizen to open a bank account in another country—even for legitimate business purposes.

It’s already very difficult. Many foreign banks no longer will do business with Americans due to the onerous reporting requirements of the U.S. Patriot Act.

Led by Michigan Senator Carl Levin, the Democrats believe foreign bank accounts allow ex-pats and others to avoid income taxes—at least $100 billion worth—and they are determined to collect it. In March 2009, Levin tried to impose new draconian rules to make it almost impossible for a U.S. citizen to open foreign bank accounts.

Find out more ways to survive the collapse of the banking system in your copy of Surviving a Global Financial Crisis and Currency Collapse. Order it today for just $19.95!

Even a Temporary Freeze on

Accounts Would Be a Disaster

What worries economists is that a large number of bank failures could overwhelm the FDIC and result in significant delays for depositors in gaining access to their savings.

If that were to happen, many Americans would be unable to pay their bills or their mortgages.

What’s more, widespread bank failures are quite possible. In the 1980s and 90s, more than 700 savings and loan institutions failed or were taken over by Federal regulators. The total cost to taxpayers was estimated at $130 billion.

Some depositors had to wait years to get their money. The Federal Savings and Loan Insurance Corporation (FSLIC) covered accounts up to the maximum of $50,000.

But depositors with large accounts often had to wait—and some never did get their money back.

Continued below…

Never, Ever Keep Gold or Cash

in a Bank Safety Deposit Box!

Bank officials have been informed by the Department of Homeland Security (DHS) that all safety deposit boxes will be seized in the event of a national disaster.

As occurred sporadically during the Great Depression, Federal agents will examine all safety deposit boxes and determine which items may be returned to bank customers. No weapons, cash, gold, or silver will be allowed to leave the bank — only paperwork will be given to its owners.

Bank officials have been instructed not to reveal this policy to bank customers, even if asked.

Bottom line: Only use safety deposit boxes for family documents you don’t mind being inspected by Federal agents. Never use them to store valuables.

Find out more ways to survive the collapse of the banking system in your copy of Surviving a Global Financial Crisis and Currency Collapse. Order it today!

And the Current Banking Crisis

is Far Worse Than the S&L

Crisis of the Early 1990s

For one thing, the current crisis doesn't just affect small savings and loans in Middle America. It's also impacting the largest banks in the world—banks like Wachovia, Citibank, Bank of America and Washington Mutual.

Each of these institutions went to Washington begging for a bailout. With hat in hand, they borrowed huge sums from the Federal government to cover bad debts worth hundreds of billions of dollars.

And while the size of these banks' bad debts is difficult to imagine, their risky nature couldn't be easier to spot. Not once you understand the nature of derivatives.

Derivatives are investments "derived" from debts—IOUs like mortgage loans, corporate bonds and credit card debts—which investment bankers bundle together and sell as investments.

It's like a collection agency buying a defaulted loan. If the debtor pays, the agency makes a profit. But if not, all it can do is write off the debt ... or else try to recoup its loss by convincing someone else to buy it.

So you can see derivatives are a far cry from offering a guaranteed return on your investment.

But the banks didn't care. After all, it was your money they were investing, not theirs. They loaded up on derivatives like a starving orphan at an all-you-can-eat buffet.

According to the Office of the Comptroller of the Currency, U.S. banks held more than $180 trillion in derivatives during the height of the financial crisis. And the Bank of International Settlements estimates the total worldwide was a staggering $683.7 trillion.

That's why, in [January 2008] , New York University economist Nouriel Roubini predicted the banking crisis was only just beginning.

Even after bailouts, consolidations and stimulus plans, we're still not out of the woods. Because bad debts aside, financial institutions aren't sure what the final tally will be on the legal troubles they face over the part they played in the financial collapse. It's a legal environment that could eventually sink them.

According to an article in The Wall Street Journal on March 2, 2011, Goldman Sachs, J.P. Morgan, Wells Fargo and Bank of America have each set aside between $1.2 billion and $4.5 billion to cover litigation stemming from possible lawsuits over the housing meltdown and other mortgage fraud claims.

And this is above and beyond what the institutions usually set aside for legal expenses.

Fortunately, there are now steps you can take to protect your life savings from the very real possibility of a global banking collapse.

In your copy of Surviving a Global Financial Crisis and Currency Collapse, I’ll help you prepare for the worst so you’ll never have to be a victim of a failed bank and unable to access your own money.

You’ll discover…

- Why the global banking system is nothing more than a massive Ponzi scheme designed to keep citizens 100 percent dependent upon government.

- The truth about the national debt and why the Federal government has no intention of ever paying it back.

- Why you should get most of your money out of banks RIGHT NOW, only keeping in enough to pay your routine bills.

- How the Fed will deliberately devalue the U.S. dollar, wiping out the life savings of millions.

- Three steps you simply MUST take right away to prepare for a global banking collapse.

- How to legally withdraw large amounts of cash from your local bank without causing suspicion.

- Why you must buy gold as fast as you can and keep it in your physical possession—and the one type of gold you should NEVER buy.

- The best type of gold coins to purchase.

- Why U.S. government bonds are the WORST possible investment you can own right now.

- The only stocks you should own in the event of a global banking collapse— and why it’s essential you hold the actual stock certificates.

- Why stockpiling durable goods is essential whenever a nation’s banking system is unsafe.

- Why you should diversify your assets outside the United States and outside the U.S. dollar.

- And lots, lots MORE!

The good news is you can FIGHT BACK and prepare to meet and overcome these threats!

Order Surviving a Global Financial Crisis and Currency Collapse!

Continued below…

WARNING: Collapse of U.S. Dollar

Could Wipe Out Half of Your Wealth!

Hyperinflation is not as rare as governments would like you to believe. Whenever a government spends far more than it takes in, the risk of hyperinflation is there. It wipes out the value of accumulated savings, leaving even affluent people penniless.

2008, Zimbabwe: The socialist dictatorship of Robert Mugabe has created an annual inflation rate of 11,250,000 percent, resulting in currency that is basically worthless. At independence in 1980, 1 Zimbabwean dollar was worth approximately $1.25 in U.S. dollars. By mid-2008, one U.S. dollar was worth 688 trillion pre-August 2006 Zimbabwean dollars.

2007, Turkey: Turkey has suffered from chronic inflation for decades. In 1980, one U.S. dollar was worth 90 Turkish lira. By 2004, a U.S. dollar was worth 1.3 million Turkish lira. As a result, in 2007 the government simply declared a revaluation of the Turkish lira. One million Turkish lira would henceforth be worth only 1 lira.

2005, Romania: In 1998, the highest denomination in Romania was 100,000 lei. By 2005, it was 1 million lei. The Romanian government then devalued its currency, declaring that 1 new leu would be worth 10,000 old lei.

2001, Argentina: Overspending by the Argentine government resulted in massive inflation in the 1980s and 90s. By 1992, one new peso was worth 100 billion pre-1983 pesos. (Had you stuffed cash in your mattress during one of Argentina’s many recessions, not trusting their shaky banks, you would have ended up with nothing.)

1994, Russia: Following the collapse of the Soviet Union, the new Russia saw annual inflation of between 2,500 percent and 8,500 percent a year. The value of the ruble declined from 40 rubles to the dollar in 1991 to 30,000 rubles to the dollar by 1999.

Don’t wait. Order your copy of Surviving a Global Financial Crisis and Currency Collapse. You’ll discover strategies and techniques that will get your wealth to safety fast!

I also want to show you…

How to Live Through the Hyperinflation

Washington Policies Are Almost Certain to Cause

In the past few months, prices have been falling. Real estate is down. Prices for some commodities have declined.

In the fall of 2010, Federal Reserve Chairman Ben Bernanke embarked on a crusade he said would revive the sluggish economy.

That’s because Barack Obama and his allies in Congress have embarked on the biggest government spending spree in history.

This socialistic expansion of government will inevitably lead to a devaluation of the U.S. dollar (hyperinflation) that could wipe out your life savings.

Imagine a world of $20 per gallon of gasoline… $30 hamburgers… and housing rentals costing $10,000 a month or more.

The economic stimulus package alone (estimated at $850 billion) is nearly DOUBLE what the U.S. spent on FDR’s New Deal in inflation-adjusted terms.

It’s 8 times more than the U.S. spent on the Marshall Plan rebuilding Europe after World War II. It’s more than we spent on NASA, the Race to the Moon or the Iraq, Vietnam or Korean Wars.

And the stimulus plan is only the tip of the iceberg!

When you add in the bailout lending for Citigroup and skyrocketing federal deficits, the U.S. government is spending $10 trillion it doesn’t have over the next few years.

Whether the government borrows it or prints it, an increase that big in the money supply is going to do only one thing: Send inflation through the roof!

The last time the U.S. government tried to spend its way out of a recession, in the 1970s, the inflation rate increased by 500% -- from a 70-year average of only 2.5% to a high of 13.5% in 1979.

But government spending in the 1970s is practically ZERO when compared to what the U.S. government is spending today.

$7.4 Trillion in New Government Debt

Will Send Inflation Skyrocketing!

In the past 12 months alone, the U.S. government (both Republicans and Democrats) has promised to spend $7.4 trillion in bailouts. According to Bloomberg.com, this includes…

… $1.8 trillion in Net Portfolio Commercial Paper Funding through the Fed…

… $1.4 trillion in FDIC Liquidity Guarantees…

… $900 billion in the Term Auction Facility (TAF)…

… $540 billion in the Money Market Investor Funding Facility (MMIFF)…

… $700 billion in the Troubled Asset Relief Program (TARP)…

… $300 billion in the Hope for Homeowners program run by the Federal Housing Administration (FHA)…

… $200 billion for the Fannie Mae/Freddie Mac bailout…

… $128 billion for the American Insurance Group (AIG) loans…

… $250 billion for Term Securities Lending…

… $139 billion loan guarantee for General Electric (GE)

That’s why you need to take steps right now to protect your retirement savings from the ravages of hyperinflation.

Currency depreciation (inflation) robs retirement pensions and all savings, but most people don’t notice because it is gradual up to the latter stages, when it is already too late.

In your copy of Surviving a Global Financial Crisis and Currency Collapse, you’ll learn some practical, real-world strategies you can put into place right now that will help you get through the worst financial catastrophe to strike America in its history.

You’ll discover…

- Why stuffing CASH in your mattress is the worst thing you can do. Do this instead.

- Why you still have TIME to prepare for hyperinflation—if you act right away.

- The right way and the wrong way to diversify your assets—and the three asset classes that are essential to surviving hyperinflation.

- The consumables most likely to be affected by hyperinflation—and which ones you should store now.

- What bankers don’t want you to know about Certificates of Deposit (CDs)

- Why hyperinflation will result in DOZENS of new taxes on the “rich”—including a hefty value added tax (VAT), as in Europe.

- How to avoid a forced conversion of savings and pension fund assets into Treasury bonds.

- Why the government will try to defeat all attempts by individuals to protect their savings and personal security.

- Why certain blue chip stocks—yes, stocks!—are a great hedge against hyperinflation.

- How to take physical delivery of stock certificates—and why it’s more important now than ever before.

- One conservative investment you should NEVER own if you’re worried about inflation.

- And lots, lots MORE!

Order Surviving a Global Financial Crisis and Currency Collapse!

I also want to show you how to…

Protect Your Family’s Privacy

from Illegal Surveillance

The U.S. Constitution protects citizens against “unlawful search and seizure.” U.S. courts have long insisted that police agencies must have “probable cause” that a crime has been committed before they can search through your home, subpoena your bank records, tap your private telephone calls, and so on.

But in the name of catching terrorists and “tax cheats,” all these constitutional protections are being flagrantly (often illegally) ignored by many government agencies.

Laws that were designed to catch terrorists are now being used instead for domestic spying in the U.S…. illegal investigations of political organizations… monitoring of bank accounts and credit card companies… routine scanning of private emails and Web browsing… tracking vehicle movements… and lots more.

Both liberal and conservative organizations are outraged at the current scope of government surveillance—which now far exceeds anything George Orwell imagined in his chilling, anti-authoritarian polemic, 1984.

Worst, the U.S. Patriot Act now requires tens of thousands of private businesses—from banks and brokerages to credit card companies and precious metals dealers—literally to spy on their customers for the government.

In the name of catching money launderers and terrorists, the government forces private businesses to report any “unusual” activity involving transactions over $3,000—and all the data is fed into a massive government supercomputer known as the Financial Crimes Enforcement Network (FinCEN).

What’s more, if employees of these businesses warn their customers about these spying activities, they could go to prison.

Continued below…

Don't Let Them Fool You:

Democrats Are Spying on Americans, Too!

President Barack Obama has done nothing to end illegal government surveillance of its citizens. In fact, it's quite the opposite.

One of Obama’s first acts as president was to file a brief in federal court siding with the former Bush Administration and insisting that the government should be allowed to eavesdrop on Americans without warrants.

Privacy advocates insist Americans will have just as much to fear from Democrat spies as they had from the Bush Administration—perhaps more.

That’s because, while George W. Bush and the Republicans trounced on civil liberties and used warrant-less wiretaps in the pursuit of global terrorists, Barack Obama and his Democrat allies are going to use the same spying technologies… on U.S. taxpayers!

“Hundreds of billions of dollars in taxes are owed to the government each year but are not being collected,” warned Rep. Charles B. Rangel, a Democrat from New York and chairman of the House Ways and Means Committee, himself investigated for criminal tax evasion.

And he should know. As you probably remember, Rep. Rangel was himself investigated and censured for failing to pay his taxes!

According to the New York Times, the kinds of “tax cheats” Obama and Congress plan on targeting include “… self-employed painters and plumbers, small family businesses (from local florists and dry-cleaners to restaurants) and the growing legions who sell things over eBay and other Internet auction sites.”

“Tax cheats come in all shapes and sizes,” explained Democratic Senator Carl Levin of Michigan, Chairman of the Senate Permanent Subcommittee on Investigations. Levin is pushing through a bill in Congress that would make offshore bank accounts virtually illegal.

“This bill contains innovative and powerful measures that could strike an immediate and strong blow against these tax dodges,” Levin said. “These provisions would recover billions that could help pay for health care, education, manufacturing support, aid for wounded warriors, and more.”

Order your copy of Surviving a Global Financial Crisis and Currency Collapse today!

You’re Guilty Until Proven Innocent

In the eyes of power-mad government bureaucrats, ordinary citizens are guilty until proven innocent—and they’re pushing for NEW, expanded police powers that will include mandatory fingerprinting, iris scans and DNA sampling of all citizens, national biometric ID cards, transponder tracking of vehicles (for mileage taxes!), even geographical tracking of citizens through microchip implants.

The potential for abuse and illegal snooping is massive—and is already occurring.

Two years ago, the U.S. Senate held hearings about possibly revoking the Patriot Act because of revelations that the FBI was routinely and illegally gathering telephone, e-mail and financial records of ordinary Americans without proper authorization.

Fortunately, there are now steps you can take—100% legal steps routinely used by Hollywood celebrities and the super-wealthy—to shield yourself from government snoops and identity thieves who want to illegally invade your privacy.

For example…

* A 100% legal way to move money offshore without violating U.S. reporting requirements. Federal law now requires that you report every bank or brokerage account you have outside the U.S. if the combined total in such accounts exceeds $10,000—or you face up to five years in prison and a fine of $500,000.

However, the wealthy have long used an investment vehicle that is exempt from such reporting requirements—offshore life insurance policies. A life insurance policy purchased from a foreign carrier is NOT considered a “foreign bank, security or other financial account” and therefore not subject to U.S. reporting laws.

What’s more, offshore insurance policies are “invisible” to the asset tracking services used by private investigators and government snoops in the U.S.

They allow you to take advantage of tax-advantaged investments and offshore funds not accessible to U.S. investors. They also enable you to diversify into non-U.S. dollar assets that may gain in the event of future declines in the U.S. dollar, economy or markets.

Best of all, offshore life insurance policies often have lower premium costs… better asset protection than their U.S. counterparts… zero tax on policy earnings… and the same provisions for tax-free borrowing and tax-free receipt of death benefit as ordinary U.S. insurance policies.

In a word: They are the perfect investment vehicle for those who want to escape the illegal prying of U.S. government snoops and predatory lawyers.

Best of all…

This Remarkably Private

Investment Is Easy!

You may think an offshore annuity sounds complicated, but it’s not. It's quick and easy. All it takes is one phone call, fax or email, and the people handling the accounts all speak excellent English.

I’ll tell you all about this amazing offshore investment in your copy of Surviving a Global Financial Crisis and Currency Collapse.

Plus, I’ll also reveal…

- How to make 100% anonymous telephone calls. Prepaid wireless cell phones (widely used in Europe and now available in the U.S.) make it impossible for government snoops to track your telephone calls. Available at many stores, these new phones don’t require credit cards, credit checks or the use of your real name. As a result, all of your phone calls are private and cannot be traced back to you or end up in a big government database.

- How to bank safely and privately within the U.S. Easy, legal steps you can take to keep your money invisible to government snoops.

- How to avoid leaving a “digital trail” with credit card purchases (and what you need to know about new anonymous prepaid credit cards).

- How to make your real estate litigation-and IRS-seizure proof. If you think a problem is suspected, foreseen or probable, you can safeguard your home, now!

- A simple way you can legally avoid probate and staggering estate taxes. This strategy lets you pass the lion's share of your wealth to your loved ones-and not to a greedy government.

- The biggest mistakes people make on their computers that leave them vulnerable to prying eyes.

- And much, much more to ensure your financial privacy as it's meant to be!

Order Surviving a Global Financial Crisis and Currency Collapse!

Plus, I want to show you…

How You Can STILL Enjoy

a Prosperous Retirement

Times of great economic upheaval present rare opportunities for investors to make enormous, staggering, life-altering profits not possible at any other time.

People forget that many fortunes were MADE during the Great Depression.

For example, Joseph Kennedy, the patriarch of the Kennedy dynasty, made his fortune during the 1930s, shorting the stock market and investing in rock-bottom real estate that soared in value after World War II.

To make money during an economic crisis, however, you have to identify hidden opportunities that others are overlooking.

How You Could Have Made 245% Profits

Over the Past Seven Years Following

Our Gold Recommendations!

If you had invested $10,000 in the S&P index at the start of 2002, you’d have seen the market plummet from 1165.27 to 712.00 by 2009— that's a total net wipeout of -38.8% over seven years.

Even today, with the S&P back to the 1200 level, when you factor in inflation, your $10,000 investment has lost money for nine years.

But if you had invested that same $10,000 in gold coins—as we recommended in January 2002 when the price of gold fell to just $275 per ounce - today your investment would be worth $52,200, less commissions.

That’s a 422% return on your money—or a 20.15% average annual return for nine years!

And here’s the good news: I’m convinced we’re going to see similar eye-popping profits in the next several years as the government depreciates the value of the U.S. dollar… inflation goes through the roof… and the price of gold continues to skyrocket.

Continued below…

A Triple-Digit Buying

Opportunity in Uranium!

There are plenty of reasons to be excited about uranium.

The dawn of the 21st century reveals a world running low on fossil fuels—and the main source in the Middle East is at high risk.

Plus, more people are aware of how fossil fuels, or hydrocarbons, are suffocating the planet! Nuclear is clean! Many Democrats in Congress and the White House now recognize this.

Also, uranium is a particularly good investment now. Prices are rising, having increased more than 50% in recent months.

But this can’t and won’t last. The world’s energy needs—combined with a new push for reducing dependence upon pollution-causing carbon fuels—will force most world governments to turn to uranium as an alternative.

Discover how you could earn TRIPLE-DIGIT profits in uranium despite the current bear market in stocks. Order your copy of Surviving a Global Financial Crisis and Currency Collapse today!

Cash in on Select Gold

and Energy Stocks!

Of course, for those people uncomfortable building a stash of Krugerands and American Eagles, you can also cash in on rising precious metals and commodities prices with select stocks.

Over the past few years, most of our stock recommendations have been in gold and silver mining companies and energy companies, including…

Up 215% in 24 months! I first recommended the uranium stock Cameco (CCO.TO) in the November 2004 issue when it was selling for around $16.41 a share. By May 1, 2007, the stock was selling for 51.70—a gain of 215% in a little over two years!

Up 145% in 36 months! I urged subscribers to buy shares of Bema Gold Corp (BGO) beginning in the September 2003 issue. It sold for around $2.98 a share back then. By the time Bema was bought by Kinross, it sold for $7.32 a share. That’s a gain of 145%.

Up 143% in 48 months! I suggested subscribers consider the energy stock BHP Billiton Ltd (BHP) when it sold for $20.10 a share. Today it sells for $88—a gain of more than 213%.

Up 120% in 36 months! Eldorado Gold Corp (EDO) sold for around $2.59 a share when I recommended it in the September 2003 issue. Three years later, it sold for $5.72 a share—a gain of 120% over three years.

Not all of our recommendations have done this well. A few have even lost money.

But in general, our gold, silver and energy recommendations have performed impressively.

And to help you cash in on what I believe will be the greatest commodities boom in history, I’ve recommended my best crisis investment recommendations in Surviving a Global Financial Crisis and Currency Collapse.

I’ll tell you about…

- Why you DON’T have to depend upon the market to systematically build your wealth.

- The secret to earning triple-digit profits in gold stocks, including my top five picks.

- An easy way to invest as much money as you want in Swiss francs without having to report it to the U.S. government (100% legal)!

- The right way and the wrong way to buy gold coins.

- Ten small gold mining stocks to consider for your long-term portfolio…

- My favorite energy stocks—and why I believe the price of oil could hit $150 per barrel in the next few months.

- Why it could soon be illegal for you to move money out of the U.S. and out of reach of the government (to stop “money laundering”).

- And lots MORE.

Order Surviving a Global Financial Crisis and Currency Collapse!

You can receive this financially lifesaving manual at introductory savings—HALF OFF!

Because I want to get this urgent 21st Century Survival Guide into the hands of as many people as possible, I've made arrangements for you to receive Surviving a Global Financial Crisis and Currency Collapse, for only $19.95—HALF off the published price.

That's right. Just $19.95 for an eBook (yes, right off your computer, right now). Order your eBook today!

Don’t be Unprepared! Discover my Simple Real-World Strategies for Building (and Rebuilding) Your Wealth During A Global Financial Meltdown!

Surviving a Global Financial Crisis and Currency Collapse is chock-full of proven strategies, techniques and information that can make all the difference in an economic emergency.

The information and strategies you discover in this eye-opening report will make your life better, even if we sidestep some of the catastrophes that I fear are coming.

That’s because the steps you take now to prepare for some of these possible disasters will end up making you financially stronger… more independent… more self-reliant… and even healthier than you are now.

Order your instant eBook of Surviving a Global Financial Crisis and Currency Collapse today!

Best wishes,

Bob Livingston

Editor, The Bob Livingston Letter®

Founded by Bob Livingston

Founded by Bob Livingston